The National Bank of Ukraine (NBU) estimates fair value of domestic government bonds:

- for recognition of domestic government bonds at fair value in line with IFRS;

- for disclosure of information on fair value of domestic government bonds in financial statements;

- for assessment of collateral adequacy for transactions with Ukrainian banks and the Deposit Guarantee Fund (DGF);

- as a benchmark for purchase/sale transactions involving domestic government bonds.

The NBU accepts domestic government bonds as collateral for the following transactions:

- refinancing

- repurchase transactions

- under agreements on storing stocks of cash

- liquidity assistance to the DGF.

In order to reduce losses caused by interest rate risk, currency risk, and liquidity risk, the NBU applies adjustment coefficients to the fair value of domestic government bonds accepted as collateral.

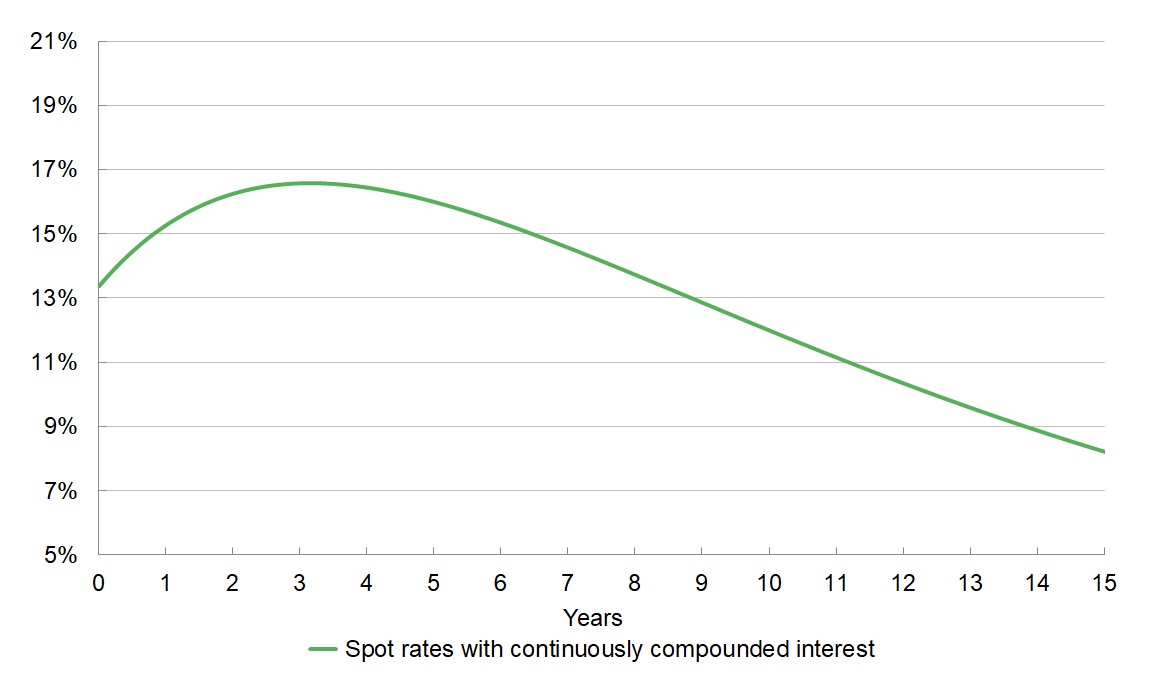

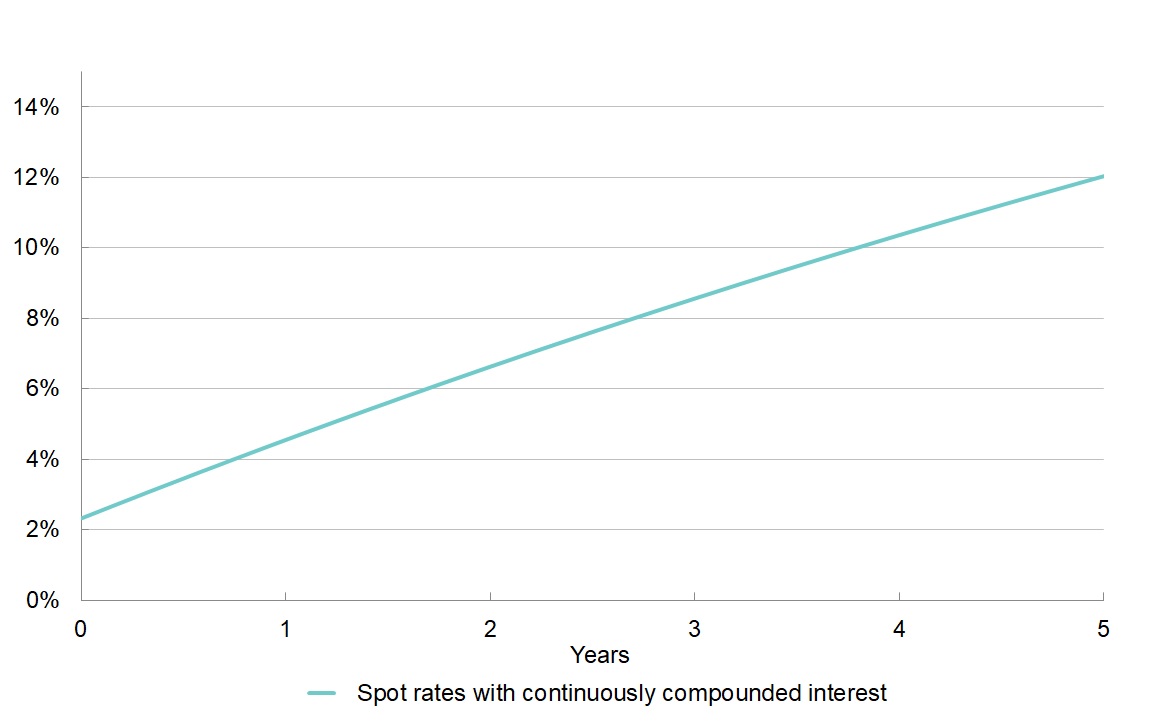

The NBU estimates fair value of domestic government bonds according to the methodology set out in the Procedure for Assessing Securities from Residents at Fair Value Held or Accepted as Security for Liabilities by the National Bank of Ukraine. The methodology complies with International Financial Reporting Standard 13: Fair Value Measurement. This methodology is based on zero coupon yield curves of domestic government bond groups that are graphic interpretations of yield of zero coupon debt securities with different maturities. The NBU plots benchmark zero-coupon yield curves of government bonds.