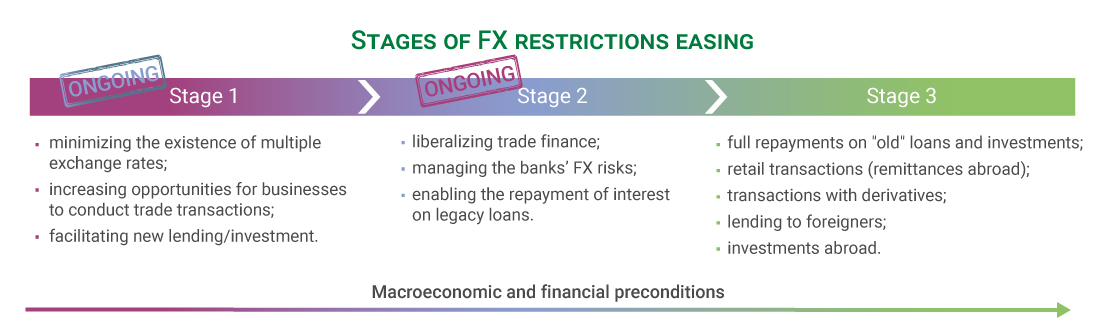

At the outbreak of the full-scale war, the NBU fixed the hryvnia’s exchange rate and imposed a number of administrative restrictions. These decisions made it possible to prevent panic and ensure the stable operation of the financial system and helped businesses and households adjust to the full-scale war. However, the fixed exchange rate regime and FX restrictions come with both benefits and costs, and over time, the costs could outweigh the benefits.

To this end, the NBU is gradually implementing the Strategy for Easing FX Restrictions, Transitioning to Greater Flexibility of the Exchange Rate, and Returning to Inflation Targeting as proper preconditions are being formed.

The steps within the stages may be reshuffled to help the economy recover and to increase the FX market’s and the financial system’s performance.

In July, the NBU published the Strategy for Easing FX Restrictions, Transitioning to Greater Flexibility of the Exchange Rate, and Returning to Inflation Targeting (“the Strategy”).

The document contains a lot of specialized terms and may be difficult to understand. This page was created to let anyone easily grasp the NBU’s plans regarding its exchange rate and monetary policies.

What does the NBU plan to do with the exchange rate and FX restrictions?